解説・まとめ

- 今回利上げ幅:0.5%利上げ

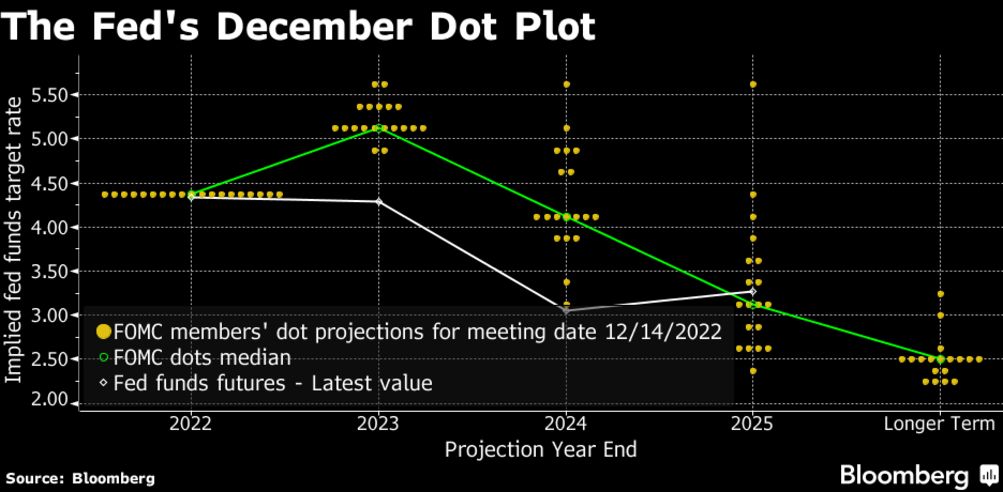

- 2023年末 金利見通し:5.00%〜5.25%(市場予想より高い)

- 利下げ時期については言及せず

- 次回利上げは0.25%の可能性を否定せず

- 今後の経済指標をもとに利上げ・利下げを行うと明言

今回利上げについて

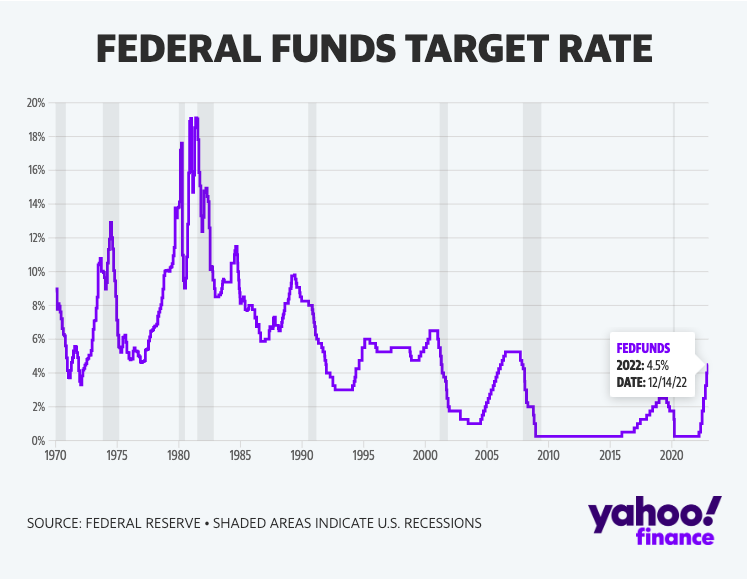

今回、政策金利を0.5%利上げを決定した。

これにより政策金利は4.25%〜4.50%となった。(下図参照)

2021年3月以降、利上げ幅は4連続で0.75%実施し0.5%の利上げ縮小は今年初となる。

利上げ幅は市場予想と一致したがパウエル議長の「2023年中の利下げはない」と発言しこのタカ派発言が2023年後半の利下げを期待していた市場にショックを与えてFOMC開催直後に株価急落。

政策金利見通しは中央値が9月時点の4.6%→来年2023年:5.00%〜5.25%に引き上げられた。

中央値は2024年末:4.1%、2025年末:3.1%

2023年まで利上げを実施し、利下げは2024年以降

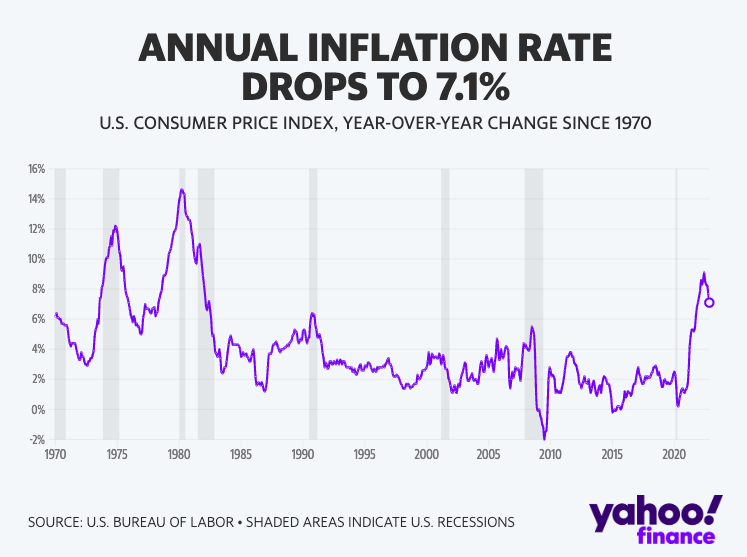

縮小を決めた背景はインフレが落ち着く兆しが出ていることがあり、12月13日に発表された11月の CPI(消費者物価指数)が前年同月より7.1%の上昇となったものの、上昇率が鈍化の兆しが見られた。

このため13日の株価は一時上昇したもの前文にて記述した通り、FOMC後に市場予想との食い違いにより下落に転じた。

FOMC主要発言抜粋

「CPI(消費者物価指数)のデータは歓迎だが、インフレが断続的に低下しているかどうかはさらに根拠が必要だ」

パウエル議長発言

「物価安定を取り戻すには長い道のりが必要あり、来年中の利下げは無い」

パウエル議長

と利下げ継続・利下げについて検討をしていない背景を説明。

その上で、

「ピーク金利はデータが悪ければ引き上げられるが、インフレ指標が軟化すれば引き下げられる」

パウエル議長

とも発言しており、このままインフレが鈍化すれば利上げ天井は想定よりもキレ下がるシナリオも十分予想できる。

要約

これまで過去のパウエル議長の発言・行動を振り返ると2022年当初の利上げタイミングや利上げ幅の対応は若干後手に回ったところもあるし、経済指標データを背景に何回も意見変更してきた経緯を考慮すると必ずしも来年2023年の利上げ実施・利下げ無しとは言い切れない。

それに加えてCPI(消費者物価指数)の抑制具合を考慮すると今回の『タカ派』な発言だったがインフレと利上げ加速については以前のような加熱レースは通り過ぎたと言えるだろう。

CPI(消費者物価指数)についてはこちらを参照ください。

全文和訳

パウエル議長 会見前の声明

こんにちは。本日の会合の詳細に入る前に。

米国国民に対して、我々は高いインフレが引き起こしている苦難を理解しており、インフレを我々の目標である2%に戻すことに強くコミットしていることを強調したい。

今年1年間、我々は金融政策のスタンスを引き締めるため、力強い行動をとってきた。私たちは多くの分野をカバーし、これまでの急速な引き締めの効果が十分に発揮されるのはこれからです。しかし、それでもまだやるべきことはあります。物価の安定は米連邦準備制度理事会(FRB)の責務であり 価格の安定は連邦準備制度の責任であり、経済の基盤として機能する。

物価の安定なくして、経済は 価格安定がなければ、経済は誰のためにも機能しません。特に、物価の安定がなければ、労働市場の好調を持続させることはできない。特に物価の安定がなければ、全ての人に恩恵をもたらす強い労働市場の状況を持続的に実現することはできない。

本日、FOMCは政策金利を1/2ポイント引き上げた。

我々は引き続き を達成するために、継続的な利上げが適切であると予想している。

インフレ率を長期的に2%に戻すのに十分な金融政策スタンスを達成するためには、継続的な引き上げが適切であると引き続き考えている。さらに、当社は バランスシートの規模を大幅に縮小するプロセスを継続しています。

物価の安定を回復するには 物価の安定を取り戻すには、しばらくの間、制限的な政策スタンスを維持する必要がありそうです。本日の金融政策については は、経済情勢を簡単に振り返った後、本日の金融政策措置について述べたいと思います。

米国経済は、昨年の急速なペースから大きく減速しています。

実質 実質GDPは前期に2.9%のペースで増加しましたが、今年1-3月期はほぼ横ばいとなっています。

最近の指標では、今期の消費と生産は緩やかに増加すると見ています。個人消費は、実質可処分所得の減少や生産量の減少を反映して、昨年の急激な伸びから鈍化しています。個人消費の伸びは、実質可処分所得の減少や金融引き締めを反映して、昨年の急激な伸びから減速しています。

住宅部門の活動は 住宅部門の活動は、主に住宅ローン金利の上昇を反映して大きく弱まりました。金利の上昇と生産高の伸びの鈍化も また、金利の上昇と生産高の伸びの鈍化が、企業の固定投資を圧迫しているようです。経済予測の概要に示すように、今年と来年の実質GDP成長率の予測中央値はわずか0.5%です。これは、長期的な正常成長率の中央値を大きく下回っています。成長率の鈍化にもかかわらず、労働市場は極めてタイトであり、失業率は50年ぶりの低水準に近く、求人倍率は依然として非常に高く、賃金上昇率も上昇しています。

雇用の増加は堅調で、過去3ヵ月間の雇用者数は月平均27万2,000人増加しました。求人倍率は過去最高を下回り、雇用増加のペースも年初より鈍化しているが、労働市場は引き続きバランスが崩れており、需要が労働力の供給を大幅に上回っている。

労働力率は年初からほとんど変化していない。FOMC参加者は、労働市場の需給状況が時間の経過とともにより良く均衡し、賃金と物価の上昇圧力が緩和されると予想している。SEPの失業率に関する予測の中央値は、来年末に4.6%に上昇する。

インフレ率は、長期的な目標である2%を大幅に上回って推移しています。10月までの12ヶ月間、PCE価格合計は6%上昇し、変動の激しい食品とエネルギーのカテゴリーを除いたコアPCE価格は5%上昇しました。11月の消費者物価指数の12ヶ月間の変動率は7.1%で、コア消費者物価指数の変動率は6%であった。10月と11月のインフレ率データは、毎月の物価上昇ペースが減少していることを歓迎している。

しかし、インフレが持続的に低下していることを確信するには、さらに多くの証拠が必要であろう。

物価上昇圧力は、幅広い商品とサービスにおいて、依然として顕著である。ロシアの対ウクライナ戦争は、エネルギーや食料の価格を押し上げ エネルギーや食料の価格が上昇し、インフレ率に上昇圧力がかかっている。

インフレ率 SEPのPCEインフレ率の中央値は、今年5.6%で、来年3.1%、2024年2.5%、2025年2.1%に低下すると予測している。参加者は引き続き、インフレに対するリスクが上昇に重きを置いていると見ている。

インフレ率の上昇にもかかわらず、長期的なインフレ期待は、家計、企業、予測担当者に対する広範な調査や金融市場の指標に反映されているように、依然として十分に固定されているように思われる。

しかし、それは自己満足の根拠にはならない。現在の高インフレが長引けば長引くほど、インフレ上昇期待が定着する可能性が高まるからだ。

FRB の金融政策措置は、米国民のために最大限の雇用と安定した物価を促進するという我々の使命に導かれている。私の同僚と私は、高いインフレが購買力を低下させ、特に食料、住宅、交通といった必需品のコスト上昇に対応できない人々にとって大きな苦難をもたらすことを痛感している。

我々は、高インフレが我々の任務の両面にもたらすリスクに強く留意しており、インフレ率を2%の目標に戻すことに強くコミットしている。

本日の会合で、委員会は連邦資金金利の目標レンジを 1/2 ポイント引き上げ、目標レンジは 4-1/4 から 4-1/2 パーセントとなった。また、我々は、バランスシートの規模を大幅に縮小するプロセスを継続している。

本日の措置により、今年4-1/4%の金利引き上げを実施したことになります。我々は、連邦預金金利の目標レンジを継続的に引き上げていくことが、金融危機を回避するために適切であると引き続き考えている。インフレ率を長期的に2%に戻すために十分に抑制的な金融政策スタンスを達成するために、フェデラルファンド金利の目標レンジを継続的に引き上げることが適切であると引き続き考えている。

今年1年間で、金融環境は以下のように変化しました。金融情勢は当社の政策に呼応して大幅に引き締まりました。金融情勢は短期的には多くの要因によって変動します。金融情勢は多くの要因に反応して短期的に変動しますが、

インフレ率を2%に戻すために行っている政策的な抑制を、長期的に反映させることが重要です。

住宅など、経済の中で最も金利の影響を受けやすい分野の需要に効果が表れています。しかし、金融抑制の効果が完全に現れるには、特にインフレ率については時間がかかると思われます。金融引き締めの累積と、金融政策が経済活動やインフレに与える影響の遅れを考慮して、委員会は本日の利上げを50bpとし、過去4回の75bpのペースから一歩後退させることを決定した。

もちろん50bpは依然として歴史的な大幅利上げであり、まだ道半ばである。

SEPに示すように、来年末の連邦資金金利の適切な水準に関する予測の中央値は5.1%で、9月の予測より1/2ポイント高い。中央値は2024年末に4.1%、2025年末に3.1%であり、長期的な値の中央値を依然として上回っている。もちろん、これらの予測は委員会の決定や計画を表すものではなく、1年以上先の経済状況を確実に知っている者はいない。私たちの判断は、入ってくるデータの全体像と、経済活動の見通しに対するその影響に左右されます。

経済活動やインフレの見通しへの影響に左右される。そして、我々は、会合ごとに意思決定を行い、我々の考えを可能な限り明確に伝え続けていく。

我々は、需要と供給がより良く一致するように、需要を緩和するための強力な手段を講じている。我々の包括的な焦点は、我々の手段を用いてインフレ率を2%の目標に戻し、長期的なインフレ期待を十分に安定させることである。インフレ率の低下には、トレンドを下回る成長率の持続と労働市場の軟化が必要となる可能性があります。物価の安定を回復することは、最大限の雇用と安定した物価を長期的に達成するための舞台を整えるために不可欠である。

歴史的な記録は、早まった政策緩和を強く戒めている。我々は、仕事が完了するまで、この方針を維持する。

最後に、私たちは、私たちの行動が全国の地域社会、家庭、企業に影響を与えることを理解しています。

我々の行動は全て、公的使命に奉仕するものである。

我々FRB は、最大限の雇用と物価安定の目標を達成するため、できる限りのことをするつもりである。

ありがとうございました。質問をお待ちしています。

質疑応答

CNBCのスティーブ・リースマン

私の質問を聞いてくださってありがとうございます、議長。

先ほど、政策抑制を市場環境に反映させることの重要性についてお話されましたが

今、議長から政策抑制を反映した市況の重要性についてお話がありました。

11月の会合以来、10年物金利は60ベーシスポイント低下し、住宅ローン金利は低下し、ハイ・イールド・クレジット・スプレッドは縮小した。住宅ローン金利は低下し、高利回り債のスプレッドは縮小し、景気は加速し、株式市場は上昇した。経済は加速し、株式市場は6%上昇した。

このような金融環境の緩和は 金融条件の緩和は、FRBがインフレと闘う上で問題となるのでしょうか? もしそうなら、何か手を打つ必要があるのでしょうか?もしそうなら、何か手を打つ必要があるのでしょうか?

また、どのように対処するのでしょうか?ありがとうございました。

パウエル議長

先ほど申し上げたように、インフレ率を2%に引き下げるために導入している政策的な抑制を、全体的な金融情勢に反映させ続けることが重要なのです。

私たちは、金融環境が過去1年間に著しく引き締まったと考えています。しかし、私たちの政策行動は金融情勢を通じて機能します。

そして、それが経済活動、労働市場、インフレ率に影響を与えるのです。

つまり、私たちがコントロールできるのは、私たちが行うコミュニケーションにおける政策の動きなのです。金融情勢は私たちの行動を予測し、それに反応します。

私たちの焦点は短期的な動きではなく、持続的な動きであることを付け加えておきます。そして、もちろん、多くの、多くのものが、時間とともに金融情勢を動かします。

今日の我々の判断では、まだ十分に制限的な政策スタンスにはなっておらず、だからこそ継続的な利上げが適切であると述べているのです。

そして、私たちの現在の評価については、もう一度SEPをご覧いただきたいと思います。ピーク水準がどの程度になるかということについては、SEPをご覧ください。

ご覧のように、今回のSEPには19名の方が記入されています。そのうちの17人が、ピーク金利を5%以上、つまり5%台と書いています。つまり、これが私たちの評価です。つまり、これが私たちが考えるピークシフトに対するベストアセスメントです。

今年に入ってからのSEPでは、ピーク金利の見積もりを増やしました。

そして今日、彼らが公表したSEPは、12月14日のことを再び示しています。

FOMC参加者は圧倒的にインフレリスクを上方修正していると考えています。ですから、次のSEPでピーク金利の見積もりが引き上げられないと自信を持って言うことはできません。 どうなるかはわかりません。今後のデータ次第です。今日書き留めたのは、現在わかっていることをもとにした、ピークレートに関する最良の推定値です。

もちろん、もしインフレ率のデータが悪化すれば、ピークレートは上昇する可能性があります。

また、インフレ率のデータが軟調であれば、下がる可能性もあります。

ニューヨーク・タイムズのジーナ・スミアレック

質問をお受けいただきありがとうございます。SEPでは、FRBは2023年にさらに3/4%ポイントの利上げを行うとしていますね。25bp刻み、50bp刻みと、そのスピードはどのように変化していくとお考えでしょうか。

そして、いつ利上げをやめるかを決めるために、何を考えているのでしょうか。

パウエル議長

そうですね。今年に入ってから、インフレの強さとその持続性を目の当たりにして、迅速に行動することが非常に重要だと思うようになりました。

実際、そのスピードとペースは最も重要なことでした。今年も終わりに近づき、今年425ベーシスポイントを引き上げ、制限的な領域に入った今、どれだけ速く動くかはそれほど重要ではありません。

それよりも、究極の水準はどこなのかを考える方がはるかに重要です。

そして、ある時点で、問題はいつまで制限的であり続けるのか、ということになります。それが最も重要な問題になるでしょう。でも、今一番大事なのは、もはやスピードではない、と私は思います。

だから、それは2月にも当てはまります。

金融情勢と経済情勢を見極めながら、今後のデータに基づいて判断することになるでしょう。

それが重要なポイントになると思いますが、つまり、その判断のために。

最終的には インフレの進捗状況、金融情勢、そして政策が十分に制限的であるかどうかを判断することになります。

今日も申し上げましたが、私たちは、今日のような状況でも、十分な制限的なスタンスにはなっていないという評価をしています。

今日の動きを見ても、十分に制限的なスタンスではないという評価をしていることをお伝えしました。そのために何をすべきか、私たちの評価を示しました。しかし、ある時点で、我々はその地点に到達することになります。そして問題は、いつまでそこに留まるかです。委員会の強い見解は、インフレが持続的に低下していると確信できるまで、そこに留まる必要があるということです。そして、それはしばらく先のことだと考えています。

では、なぜそんなことを言うのか。

インフレを3つのバケツに分類することができます。

1つ目は財のインフレで、私たちが1年半前から予想していたように、供給状況が良くなっていることがわかります。

そして、最終的にはサプライチェーンが固定化され、需要が少し落ち着き、サービス業に少し戻るかもしれません。そして、商品インフレが低下し始めるのです。

インフレ率も下がってきます。今回のレポートと前回のレポートでは、それが見え始めています。

2つ目は、住宅サービスです。住宅サービスのインフレ率は非常に高く、今後も上昇し続けることが予想されます。しかし、新しいリースのレートは下がってきています。

ですから、この残債を処理すれば、来年にはインフレ率は下がると思います。

3つ目は、PCEコア・インフレ・インデックスの55%を占める非住宅関連コア・サービスです。このセクターで最も大きなコストは人件費で、これは労働市場の機能です。労働市場は非常に好調で、雇用の伸びは非常に高く、賃金も非常に高いです。

空室率はかなり高く、労働市場では需要と供給のバランスが崩れています。

ですから、この部分が一番大きいのですが、これを下げるには相当な時間がかかると思われます。もうひとつは……財のインフレは、1年半ほどまったく転じていなかったのに、今はかなり急速に転じていますね。1年半ほどはまったく変化していませんでしたが、今は変化しているようです。

しかし、サービスインフレはそれほど早くは下がらないだろうという予想があり、そうなると利上げをしなければならないかもしれません。そのため、私たちは高金利を記録し、しばらくは高金利を維持しなければならないと予想しています。

ロイターのハワード・シュナイダー

質問をお受けいただきありがとうございます。あなたは、SEPのGDP成長率を「緩やか」あるいは「控えめ」と表現していると思います。しかし、実際には失速のスピードに近づいています。

半減は大したことではありません。労働市場の失業率については、いくらか軟化していると説明されました。しかし、ほぼ1%ポイントの上昇です。

これは歴史的に不況とされてきたことをはるかに超えています。なぜFRBはこれを景気後退の予測とは考えないのでしょうか?

パウエル議長

さて、予想についてお話しします。プラス成長なので、リセッションとは言えないと思います。

SEPの予測は、基本的には、あなたが言ったように、控えめなレベルの成長、つまり、0.5%ポイントのプラス成長ということです。しかし、これは低成長です。トレンドを大きく下回っています。好景気という感じではありません。非常にゆっくりとした成長という感じでしょうか。

そのような状況下で、労働市場の状況は少し軟化しています。失業率は少し上がります。多くのアナリストは、現時点では自然失業率が実は上昇していると考えていると言っていいでしょう。

ですから、これらの予測やインフレが本当に自然失業率を大きく上回っているかどうかはわかりません。その位置を正確に特定することは決してできません。しかし、4.7%というのは依然として強力な労働市場です。現場からの報告では、ハイテク企業を除けば、企業は解雇に消極的で、これはまた別の話です。一般に、企業は今いる労働者を手放したくないのです。なぜなら、採用が非常に難しいからです。

だから、雇用者数をはるかに超える数の空席があるわけです。これは、多くの人を失業させなければならないような労働市場とは思えません。ですから、労働市場が比較的緩やかな失業率の上昇で均衡を取り戻せるような経路があるはずです。

そのどれもが保証されているわけではありませんが、彼らの予測はそうなっています。

ウォール・ストリート・ジャーナルのニック・ティミラオス

パウエル議長、ジーナの質問のフォローをしたい。利上げのペースを落とすという決定、つまり利上げは、公式化されたようだ。前回の会合では、過去2回のCPI報告でインフレ率が低下する前に、ほぼ社会的に決定されたようだ。インフレ率は委員会の予測に沿って減速していることが示されました。

今、あなたは政策のタイムラグに注意するように言っています。

それは つまり、すべての条件が同じであれば、25ベーシスポイントずつ動かして、終値がどこにあるのかを探る方が安心ということでしょうか。25ベーシスポイント刻みで動くことで、次回の会合から始めることも含めて、終値がどこにあるのかを探る方が安心だということでしょうか。

パウエル議長

ですから、前回の会合でどの程度の利上げを行うかについては、まだ判断していません。しかし、あなたがおっしゃったことはおおむね正しいと思います。つまり、これほど早く動き、これほど多くの抑制策がまだ準備されているのですから、今行うべきことはゆっくりとしたペースに移行することだと考えています。

そうすることで、私たちは自分たちのやり方を理解し、そのレベルに達することができ、私たちが直面するリスクとよりよいバランスをとることができると思います。

これがその考え方です。特に、これまでの道のりを考えると、とても理にかなっていると思います。しかし、繰り返しになりますが、実際の規模がどの程度になるかは、今日お話しすることはできません。特に、経済状況や金融情勢など、今後入ってくるデータなど、さまざまな要因に左右されるでしょう。

ウォール・ストリート・ジャーナルのニック・ティミラオス

もし先週CPIが発表されたなら、その結果によって本日の予想に変更があったと思いますか?

パウエル議長

いいえ、まったくありません。慣例として、SEPはどんなデータも反映します。

会議中に発表されるあらゆるデータを反映させます。参加者は、会議中にSEPを変更できることを知っていますし、記者会見のかなり前に変更すれば、私たちが走り回ることもなくなります。しかし、そうではありません。会議の初日に入った重要なデータがSEPに反映されていないということは決してないのです。

ワシントン・ポストのレイチェル・シーゲル

質問をお受けいただきありがとうございます。失業率の予想についてお話いただければと思います。なぜFRBは失業率の見通しを引き上げたのでしょうか?末端金利が上昇すれば、自動的に失業率も上昇するとモデルが示唆しているからでしょうか?

それとも、労働市場が今思っているほど強くないという兆候を見ているのでしょうか?

ありがとうございます。

パウエル議長

いいえ、労働市場の強さについてではありません。労働市場は明らかに非常に強いです。それよりも、今までに、私たちはインフレの進展が実際よりも速くなると予想し続けてきたのです。そのため、今年のピークレートは、今回の会合と9月の会合の間で上昇しています。インフレの進展が予想より遅れていることがわかります。

だからインフレ率が上がるのです。だから失業率が上がるのです。もっと政策を引き締めなければならないからです。だから、今回の会合で失業率はそれほど上がらなかったと思います。しかし、インフレの進展が遅く、政策が引き締まり、金利が上がり、インフレ率を2%に下げるために必要な制限を受けるために、金利が長く維持されるかもしれない、ということです。

ワシントン・ポストのレイチェル・シーゲル

この数字を達成するために、レイオフや欠員、人員削減、労働力人口の変化などがどの程度原因になっているか、把握していますか?

労働力人口比率の変化によるものなのでしょうか。

パウエル議長

非常に言いにくいのですが。歴史を見ればわかることです。そして、歴史は、このような状況では、失業率の低下の方が、そこに書かれていることよりも意味があると言うことでしょう。しかし、なぜそう考えるのでしょうか?いくつか理由を挙げてみましょう。まず第一に、空室が大量に発生しているため、空室が相当数減少する可能性があるということです。

そして、多くの企業が、あまりに厳しい状況なので、解雇せずに人材を確保したいと言っています。つまり、労働力不足は構造的なもので、労働力の需要に対して、働ける人が400万人(400万人強)少なくなっているのだと思います。つまり、労働市場が強いということは、企業が労働者を確保することを意味します。

つまり、時間がかかるかもしれませんが、失業にかかるコストが少なくなる可能性があるということです。

でも、これは合理的にあり得る結果だと思います。多くの労働経済学者がそう考えているようです。 というわけで、いずれわかることでしょう。

フィナンシャル・タイムズのコルビー・スミスです。

SEPの2023年のコアインフレ率の上昇予測をどう解釈すべきでしょうか?そうすると、現在予測されている来年の政策金利は、5.1という中位推計よりも実際に高くなるはずだということになりませんか?

パウエル議長

そうですね、上昇した理由のひとつは、今年、コアがより強くなったことだと思います。そうです。

ここにあるのは、今日現在、金利をどれだけ上げれば、経済活動を減速させ、労働市場を軟化させ、その経路を通じてインフレ率を低下させるに十分な、つまり制限的な政策を作り出すために、どれだけ政策を引き締めればよいかという我々の最善の推定値です。

これが今日私たちが行った見積もり、ベストエスティメイトのすべてです。

そして、先ほど申し上げたように、次のSEPでは別の推計を行う予定です。

もちろん、会議の合間にも同じことをしますが、公表はしません。

ポリティコのビクトリア・グイダ

SEPで何が起こっているのか、具体的に理解したいと思います。皆さんは金利が上がると予想していますが、来年のインフレについてもより悲観的です。インフレ率の冷え込みが見られるということですが、それは主に賃金の伸びが原因なのでしょうか、賃金の伸びがある種の逆風になると予想しているのでしょうか。

パウエル議長

来年は、私たちが考えていたよりも高いインフレ率で迎えることになりますね。

つまり、来年のインフレ率は、現在のインフレ率から1%以上低下しているのです。しかし、年初のジャンプオフポイントはもっと高いことを忘れないでください。

しかし、年初のインフレ率の方が高いことを忘れないでください。政策の効果が落ちているとは思えません。2022年末の時点でより高い水準からスタートしているだけなのです。だから、下がってきているのです。中央値は3.5%だと思います。ということは、かなりインフレ率が下がっていることになりますね。

そして、それはどこから来ているかというと、明らかに商品部門からきています。来年の半ばには、住宅サービスセクターのインフレ率が下がり始めるはずです。そして、大きな問題は、最大の、つまり指数の55%を占める非住宅サービス部門から、いつどれだけのインフレが発生するかということです。そこで必要なのは、労働市場における需要と供給のバランスをより良くすることです。

強力な賃上げを望んでいるのです。ただ、2%のインフレ率に見合ったレベルであってほしいのです。

今、生産性推計を考慮すれば、標準的な生産性推計を考慮すれば、賃金は2%のインフレと一致する水準をはるかに超えているのです。

Axiosのニール・アーウィン

あなたの同僚の中には、2023年に利下げが行われるとは考えられないとはっきり言う人もいますね。確かにSEPはそれを暗示していない。

しかし、先物市場は来年後半の緩和を織り込んでいる。

来年の利下げの可能性についてはどうお考えですか。

また、どのような状況であれば、その可能性が高いと思われますか。

パウエル委員長

今、私たちが重視しているのは、インフレ率を長期的に2%の目標に戻すために、政策スタンスを十分に制約的なものにすることです。

金利引き下げではありません。そして、しばらくは制限的な政策スタンスを維持しなければならないと考えています。歴史的な経験から、早まった政策緩和を強く戒めています。このように言えると思います。インフレ率が持続的に2%まで低下すると委員会が確信するまでは、利下げを検討することはないでしょう。というのが、私の考えるテストです。そして、あなたの言うとおりです。2023年のSEPには利下げは入っていません。

ブルームバーグのスティーブ・マシューズ

中国についてお聞きします。ここ数週間、中国はCOVID政策を放棄し、かなり強力に再開しています。

サプライチェーンが改善されていることからディスインフレと見ているのか、それとも明らかに世界的に多くの需要をもたらし、成長と商品価格の世界的な見通しを証明することからインフレと見ているのか、疑問に思っています。

パウエル議長

ですから、あなたの言うとおりです。この2つは互いに相殺されるでしょう。中国の生産量低下は商品価格を押し下げますが、最終的にはサプライチェーンに支障をきたす可能性があり、それが欧米のインフレ率を押し上げる可能性があります。

この2つがどの程度、どのように相殺されるかは、非常に難しいところです。そして、全体的な正味の効果が私たちに重大な影響を与えるとは、実際には思えません。しかし、ご指摘のように、中国は再開に向けて非常に困難な状況に直面しています。COVIDの波が経済活動の妨げになることは、世界中で起きていることです。中国は、製造と輸出のための非常に重要な製造拠点です。

製造と輸出のための非常に重要な製造拠点です。そのサプライチェーンは非常に重要です。そして中国は再開に直面しています。彼らはCOVID規制政策から手を引きましたが、それはCOVIDを非常に大きく増加させる可能性があります。

これは非常に大きな増加要因です。危険な状況です。しかし、繰り返しになりますが、私たちに重大な全体的影響を及ぼすとは思えません。

AP通信のクリス・ラガーバー

私の質問に答えていただき、ありがとうございます。昨日のインフレレポートについて、もう少しコメントいただけないでしょうか。つまり、ブルッキングスであなたが示した3つのカテゴリーすべてにおいて、インフレが冷え込んでいることを示しています。インフレをコントロールするための真の進歩が見られると確信し始めていますか?

それとも、インフレが定着しないまま上昇スパイラルに陥ることをまだ懸念していますか?

ありがとうございました。

パウエル議長

そうですね。10月と11月のデータは、11月のデータがまだ残っていますが、明らかに毎月の物価上昇のペースが減少していることがわかります。

冒頭で申し上げたように、インフレが持続的に低下していることを確信するには、さらに多くの証拠が必要です。

つまり、私たちはこのように考えています。このレポートは、私たちが期待し望んでいたものと非常によく一致しています。そして、この報告書がもたらすものは、インフレ率の低下という我々の予測にさらなる確信を与えるものであるということです。先ほど申し上げたように、私たちは

来年はインフレ率全体とコア・インフレ率が大幅に低下すると予想してきました。その裏付けとなるのが、このような数値なのです。ですから、この時点で予想を変更するのではなく、予想に大きな自信を与えるものです。サプライチェーンの圧力が緩和され、インフレ率が下がると予想していました。

今、それが起こっています。住宅サービスについては、先ほど申し上げたように、良いニュースがあります。

住宅サービスでは、先ほど申し上げたように、良いニュースがあります。住宅、つまり新築住宅のリースがインフレ率の低下を示している限り、それは来年の半ば頃に指標に現れるでしょう。これは助けになるはずです。そして、やはりコア・サービス、X住宅は非常に重要です。これは非常に重要で、まだ道半ばです。この点については、まだ道半ばです。しかし、最終的には、PCEコア指数の半分以上を占めるのは、先ほど申し上げたように、このコアサービスです。そして、それは非常に基本的に労働市場と賃金に関するものです。賃金を見ると、前回の雇用統計で示された平均時給の数字を見ると、平均時給が下がっているという点で、あまり進展が見られません。構成効果や他の効果もあるかもしれません。ですから、1つの報告書をあまり重要視しないようにしましょう。こうしたことは月ごとに不安定になりがちです。しかし、私たちは、賃金が、労働者がうまくやっていて、結局のところ、彼らの利益がインフレに食い潰されていない、より正常なレベルまで下がっていくことを見ていくことになるでしょう。

ブルームバーグ・ラジオ&テレビのマイケル・マッキー

先ほどの経済に関する楽観的な見方と、SEPで行った変更との間には、少々食い違いがあるようですね。

経済に関するあなたの楽観的な見方と、あなたがSEPで行った変更との間に、少しずれがあります。市場が金融情勢を緩めたことに反応しているのか、それともFRBがインフレに対して少し遅れていると感じているのか、最近見られるディスインフレが一過性のものかどうか、今年の成長率をわずか50%程度と予測しているのであれば、これがソフトランディングという考えにどう影響するのか、気になるところです。

パウエル議長

ご質問はわかりました。ひとつ言えることは、私たちの政策は今、かなり良い状態にあるということです。制限的であり、十分なレベルに近づいていると思いますし、十分に制限的だと思います。今日、そこに到達するための最良の推定値を示しました。つまり、このプロセスにどれだけの時間がかかると考えているのか、ということに尽きます。

もちろん、過去2ヶ月間のインフレ報告が改善されたことは歓迎すべきことです。非常に喜ばしいことです。しかし、私たちはより広範なプロジェクトについて現実的だと思います。

以上です。これが私の言いたいことです。つまり、私たちは商品価格が下がっていくのを見ているのです。住宅サービスがどうなるかは理解しています。

しかし、大きな話題となるのはそれ以外の部分であり、そこではあまり進展がありません。私や同僚の見解では、これはしばらく時間がかかると思います。私たちは持続的に制限的な水準で政策を維持しなければならないので、2つの良い月次報告があれば、とても歓迎されます。もちろん、大歓迎です。

しかし、私たちは自分自身に正直になる必要があります。12ヶ月のコアインフレ率はCPIで6%です。これは目標の2%の3倍にあたります。今、進歩が見られるのはいいことです。

しかし、物価の安定に戻るには長い道のりがあることを理解しましょう。

マイケル・マッキー

ソフトランディングはもはや達成不可能だとお考えですか?

パウエル議長

いいえ、そんなことは言いません。そうとは言いません。つまり、こう言いたいのです。金利を高く保ち、それを長く維持する必要があり、インフレ率がどんどん上昇すれば、その分滑走路が狭くなると思います。しかし、インフレ率の低下が長引けば、その可能性はより高まるでしょう。ですから、景気後退が起こるかどうか、起こったとしてもそれが深刻なものになるかどうかは誰にもわからないと思います。ただ、それはわからないのです。インフレ率の低下が一定期間続くと、物価の安定が回復し、失業率の上昇が過去の記録から予想されるよりも大幅に抑制される可能性が高くなります。

Brian Cheung, NBC

ニュースです。あなたは今年初め、FRBが金利を上げるとアメリカ人が苦しむと警告しました。しかし、FRBはあなたが最初にそう言ったときに考えていたよりも高い金利を上げると予想されており、私たちの痛みはどこにあるのかと思っています。もし失業率が予想通りになったら、160万人のアメリカ人が職を失うことになりますが、そのことをアメリカ人にどう説明しますか?

パウエル議長

つまり、最大の痛み、最悪の痛みは、十分に高い金利を上げることができず、インフレが経済に定着するのを許してしまい、経済からインフレを取り除くための究極のコストが、雇用の面で非常に高くなり、つまり長期にわたって非常に高い失業率が続くことから生じるでしょう。もし私たちが行動を起こさなかったとしたら、それは本当に最悪の痛みとなるでしょう。今、私たちがしていることは、人々の金利を上げることです。人々は住宅ローンやその類のものに対して高い金利を支払っているのです。

ということです。労働市場の状況も多少軟化するでしょう。

物価の安定を取り戻すのに全く痛みを伴わない方法があればいいのですが、それはありません。

しかし、それは無理です。そして、これが私たちにできる最善の方法です。しかし、私は、私たちがインフレをコントロールできると、市場はかなり自信を持っているように思います。インフレはコントロールできると思います。

私はそう信じています。私たちはそのために強くコミットしています。

フォックスビジネスの グレイディ・トリンブル

あなたは今日、委員会が2%のインフレ目標へのコミットメントを繰り返し表明しました。もし、その目標があなたの考えているよりも厳しいものであった場合、その目標を見直し、インフレ目標を引き上げるようなことはあるのでしょうか?

パウエル委員長

それは、インフレ目標を変更するというのは、私たちが考えていないだけで、考えるつもりもないことです。2%のインフレ目標があり、インフレを2%に戻すために手段を講じる、ということです。

今はそのことを考える時期ではないと思います。つまり、長期的なプロジェクトがあるのかもしれません。しかし、それは我々が今いる場所には全くない。

委員会、そんなの検討してないですよ。どんなことがあっても、それを検討するつもりはありません。インフレ目標を2%に維持するつもりです。を2%に維持します。インフレ率を2%に戻すために我々の手段を使うつもりです。

CNNビジネス、ニコール・グッドキンド

賃金の伸びと失業率のデータをモニターする際、セクターや所得水準にまで細心の注意を払っているのでしょうか?特に2020年のK字型回復を考えると、不平等が悪化する可能性をどのようにリスク計算に織り込んでいるのでしょうか?

パウエル委員長

2018年、19年、20年にあった労働市場に立ち返ります。

それはどうだったかというと、所得が一番低い人たちの賃金の上昇が一番大きかった。人種間、男女間の格差は記録史上最小となりました。

インフレ率が2%をわずかに下回り、経済が潜在成長力の範囲内で成長したのは、労働市場が逼迫していたからです。このような状態に戻ることができれば、経済や国にとって本当に良いことだと思うのです。私たち全員が望んでいることです。労働市場が長期間にわたって好調を維持できるような、長い景気拡大に戻したいのです。それは労働者にとって本当に良いことです。短期的には、物価の安定を回復するために手段を講じなければなりません。しかし、私たちが考えなければならないのは、中長期的なことです。中長期的なことを考えなければならないのです。しかし、中長期的なことを考えなければなりません。私たちの想像をはるかに超える困難な時期を過ごしたと思います。しかし、そのおかげで しかし、そのおかげで、数十年にわたる経済的繁栄が実現したのです。ですから、物価の安定は、本当に 物価の安定は、非常に長い期間にわたって、経済と人々の利益のために配当されるものです。ということです。

ですから、何らかの理由で失われた場合、できるだけ早く回復させなければなりません。それが、私たちが行っていることです。

ニコル・グッドカインド

短期的には、経済の悪化や潜在的な悪化は織り込み済みですか?

経済が悪化する可能性を考慮していますか?監視していますか?

パウエル議長

はい、しています。絶対にそうします。私たちは、人種別などさまざまなグループ別の失業率について話すことを常日頃から行っています。

そのようなことをします。そうです。私たちはそれを注視しています。

マーケットプレイスのナンシー・マーシャル=ゲンザー

もし経済が大きく減速して、インフレが減速しているという一貫した強い兆候が現れる前に不況に突入してしまったら、つまりスタグフレーションになってしまったらどうするのですか?

パウエル委員長

ですから、あまり多くの仮説に立ち入りたくないのです。でも、難しいですね。仮定の話をするのは難しいのです。だから、私たちは最大限の雇用と物価の安定を支えるために

最大限の雇用と物価の安定を支えるための手段を使わなければなりません。今、労働市場は非常に好調で、50年ぶりの低水準に近く、最大限の雇用を維持しているか、それ以上であることは明言してきました。失業率は50年ぶりの低水準で、空室率は非常に高く、賃金も名目賃金が非常に高い。つまり、労働市場は非常に強いのです。不足しているのはインフレの面です。そして、インフレの面では、かなり大きな差があります。つまり、インフレをコントロールすることに焦点を当てる必要があり、それが私たちの仕事です。経済が回復すれば、この2つの目標はより重要な意味を持つようになると思います。しかし、今は明らかに、インフレを抑えることに焦点を当てなければなりません。

MarketWatchのGreg Robb

先ほど、少しお話を伺いました。アメリカは経済的に構造的な労働力不足に陥っているように見えるとおっしゃいましたね。それについてもう少し詳しく説明していただけますか?もう少し詳しく話してください。そして、本当に、合法的な移民を増やすために、議会に行動を起こさせることについて話しているのでしょうか?

ありがとうございました。

パウエル議長

構造的な労働力不足ということですが、現在の状況を見ると、先ほど申し上げたように、労働力の需要だけを見ると

空席と実際に働いている人の数です。そして、労働市場にいるかどうかで労働力の供給を考えることができます。仕事を探しているのか、仕事を持っているのか。その結果、400万人以上が不足していることがわかりました。賃金が非常に高く、労働市場が非常にタイトであるにもかかわらず、労働参加率が上がっていないのは、私たちが考えていたことと正反対です。つまり、労働市場は、パンデミック前に想定されていたよりも、少なくとも350万人少なくなっているのです。人口とそれなりの成長、高齢化を前提にすれば、労働力は現状より350万人多くなるはずです。さらに数年さかのぼれば、もっと大きな数字になることは簡単です。では、なぜなのでしょうか。その理由の一つは、退職が加速していることです。退職した人が予想以上に戻ってきていないのです。50万人近く働いていたはずの人がCOVIDで亡くなったことも一因でしょう。

また、移住者が減少していることも一因です。私たちは処方箋を出すのが仕事ではありません。しかし、企業に尋ねると、ほとんどの人が、人が足りないと言います。もっと人が必要だ」と。1カ月前に行ったスピーチで、この点を指摘しようとしましたが、議会が我々に仕事を与えてくれたので、何をすべきかを指示するのは止めました。私たちはその仕事をしなければならないのです。

ありがとうございました。

ヤフー・ファイナンスのジェニファー・ションバーガー

あなたは、来年の成長率はわずか1/2パーセントと予想しています。

利上げとインフレ抑制のプロセスは痛みを伴うと述べています。委員会の中で、どれくらいの期間、どれくらいの深さの景気後退を受け入れることができるのか、議論したのでしょうか?

パウエル議長

いいえ、私たちが行っているのは、予測を立て、四半期ごとに発表することです。

四半期ごとに発表しています。そして、これらの予測を見ると、低成長、労働市場の軟化、つまり、失業率は上がるがそれほどでもないという予測になっています。そして、インフレ率は下がる。金利は上がります。インフレ率は下がります。これらの予測は、まさにそれを示しています。私たちはもちろん、こういう不況だ、ああいう不況だと言っているわけではありません。

私たちは予測を立てているのです。スタッフは、古いTealbooksを見ればわかりますが、あらゆる種類の代替シミュレーションを毎回の会議で行っており、私たちはそれらも見ています。そして、そのシミュレーションによって、さまざまなことが検討されます。しかし、これはあくまでも、上向きと下向きのシナリオです。もちろん、これは何十年も続けてきた責任あるやり方です。しかし、私たちはそのような質問をしたことはありません。

マーケット・ニュースのジーン・ユン

SEPについてもう一度お聞きしたいのですが。来年前半に5%前後のピーク金利に達し、インフレ率が実質的に低下し始めるとすれば、実質金利は次第に制限的になるように思われますが、いかがでしょうか。そのようなことは予測やモデルに組み込まれているのでしょうか。それは、あなたが見たいと思うものですか?

パウエル議長

ですから、それはわかっています。もちろん、そのようなことが起こることは分かっています。

しかし、先ほど申し上げたように、インフレが持続的に低下していると確信できるまでは、委員会が金利を引き下げるとは思えません。それが私のテストです。中立金利と実質金利について明確で正確な理解を持っているとは思えませんので、そのようなことが機械的に起こるとは思えません。金利を下げるかどうかは、インフレが持続的に低下しているという確信が持てるかどうかが問われることになると思います。

ありがとうございました。

英文

December 14, 2022 Chair Powell’s Press Conference

Transcript of Chair Powell’s Press Conference

CHAIR POWELL.

Good afternoon. Before I go into the details of today’s meeting, I would like to underscore for the American people that we understand the hardship that high inflation is causing and that we are strongly committed to bringing inflation back down to our 2 percent goal. Over the course of the year, we have taken forceful actions to tighten the stance of monetary policy. We have covered a lot of ground, and the full effects of our rapid tightening so far are yet to be felt. Even so, we have more work to do. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy doesn’t work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. Today, the FOMC raised our policy interest rate by 1/2 percentage point. We continue to anticipate that ongoing increases will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In addition, we are continuing the process of significantly reducing the size of our balance sheet. Restoring price stability will likely require maintaining a restrictive policy stance for some time. I will have more to say about today’s monetary policy actions after briefly reviewing economic developments. The U.S. economy has slowed significantly from last year’s rapid pace. Although real GDP rose at a pace of 2.9 percent last quarter, it is roughly unchanged through the first three quarters of this year. Recent indicators point to modest growth of spending and production this quarter. Growth in consumer spending has slowed from last year’s rapid pace, in part reflecting lower real disposable income and tighter financial conditions. Activity in the housing sector has weakened significantly, largely reflecting higher mortgage rates. Higher interest rates and slower output growth also appear to be weighing on business fixed investment. As shown in our Summary of Economic Projections, the median projection for real GDP growth stands at just 0.5 percent this year and next, well below the median estimate of the longer-run normal growth rate. Despite the slowdown in growth, the labor market remains extremely tight, with the unemployment rate near a 50-year low, job vacancies still very high, and wage growth elevated. Job gains have been robust, with employment rising by an average of 272,000 jobs per month over the last three months. Although job vacancies have moved below their highs and the pace of job gains has slowed from earlier in the year, the labor market continues to be out of balance, with demand substantially exceeding the supply of available workers. The labor force participation rate is little changed since the beginning of the year. FOMC participants expect supply and demand conditions in the labor market to come into better balance over time, easing upward pressures on wages and prices. The median projection in the SEP for the unemployment rate rises to 4.6 percent at the end of next year.

Inflation remains well above our longer-run goal of 2 percent. Over the 12 months ending in October, total PCE prices rose 6 percent; excluding the volatile food and energy categories, core PCE prices rose 5 percent. In November, the 12-month change in the CPI was 7.1 percent, and the change in the core CPI was 6 percent. The inflation data received so far for October and November show a welcome reduction in the monthly pace of price increases. But it will take substantially more evidence to give confidence that inflation is on a sustained downward path. Price pressures remain evident across a broad range of goods and services. Russia’s war against Ukraine has boosted prices for energy and food and has contributed to upward pressure on inflation. The median projection in the SEP for total PCE inflation is 5.6 percent this year and falls to 3.1 percent next year, 2.5 percent in 2024, and 2.1 percent in 2025; participants continue to see risks to inflation as weighted to the upside. Despite elevated inflation, longer-term inflation expectations appear to remain well anchored, as reflected in a broad range of surveys of households, businesses, and forecasters, as well as measures from financial markets. But that is not grounds for complacency; the longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched. The Fed’s monetary policy actions are guided by our mandate to promote maximum employment and stable prices for the American people. My colleagues and I are acutely aware that high inflation imposes significant hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2 percent objective.

At today’s meeting the Committee raised the target range for the federal funds rate by 1/2 percentage point, bringing the target range to 4-1/4 to 4-1/2 percent. And we are continuing the process of significantly reducing the size of our balance sheet. With today’s action, we have raised interest rates by 4-1/4 percentage points this year. We continue to anticipate that ongoing increases in the target range for the federal funds rate will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. Over the course of the year, financial conditions have tightened significantly in response to our policy actions. Financial conditions fluctuate in the short term in response to many factors, but it is important that over time they reflect the policy restraint we are putting in place to return inflation to 2 percent. We are seeing the effects on demand in the most interest-sensitive sectors of the economy, such as housing. It will take time, however, for the full effects of monetary restraint to be realized, especially on inflation. In light of the cumulative tightening of monetary policy and the lags with which monetary policy affects economic activity and inflation, the Committee decided to raise interest rates by 50 basis points today, a step down from the 75-basis point pace seen over the previous four meetings. Of course, 50 basis points is still a historically large increase, and we still have some ways to go. As shown in the SEP, the median projection for the appropriate level of the federal funds rate is 5.1 percent at the end of next year, 1/2 percentage point higher than projected in September. The median projection is 4.1 percent at the end of 2024 and 3.1 percent at the end of 2025, still above the median estimate of its longer-run value. Of course, these projections do not represent a Committee decision or plan, and no one knows with any certainty where the economy will be a year or more from now. Our decisions will depend on the totality of incoming data and their implications for the outlook for economic activity and inflation. And we will continue to make our decisions meeting by meeting and communicate our thinking as clearly as possible. We are taking forceful steps to moderate demand so that it comes into better alignment with supply. Our overarching focus is using our tools to bring inflation back down to our 2 percent goal and to keep longer-term inflation expectations well anchored. Reducing inflation is likely to require a sustained period of below-trend growth and some softening of labor market conditions. Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run. The historical record cautions strongly against prematurely loosening policy. We will stay the course, until the job is done. To conclude, we understand that our actions affect communities, families, and businesses across the country. Everything we do is in service to our public mission. We at the Fed will do everything we can to achieve our maximum employment and price stability goals.

Thank you. I look forward to your questions.

Steve Liesman, CNBC.

Thanks for taking my question, Mr. Chairman. You just talked about the importance of market conditions reflecting the policy restraint you put in place. Since the November meeting, the 10-year has declined by 60 basis points, mortgage rates have come down, high yield credit spreads have come in, the economy’s

accelerated, and the stock market’s up 6 percent. Is this loosening of financial conditions a problem for the fed in its effort and its fight against inflation? And, if so, do you need to do something about that? And how would you do something about that? Thank you.

CHAIR POWELL

So, as I mentioned, it is important that overall financial conditions continue to reflect the policy restraint that we’re putting in place to bring inflation down to 2b percent. We think that financial conditions have tightened significantly in the past year. But our policy actions work through financial conditions. And those, in turn, affect economic activity, the labor market, and inflation. So what we control is our policy moves in the communications that we make. Financial conditions both anticipate and react to our actions. I would add that our focus is not on short-term moves but on persistent moves. And many, many things, of course, move financial conditions over time. I would say it’s our judgment today that we’re not at a sufficiently restrictive policy stance yet, which is why we say that we would expect that ongoing hikes would be appropriate. And I would point you to the SEP again for our current assessment of what that peak level will be. As you will have seen, 19 people filled out the SEP this time, and 17 of those 19 wrote down a peak rate of 5 percent or more, in the 5’s. So that’s our best assessment today for what we think the peak rate will be. You will also know that, at each subsequent SEP during the course of this year, we’ve actually increased our estimate of what that peak rate will be. And today we’re the SEP they were published shows again that overwhelmingly FOMC participants believe that inflation risks are to the upside. So I can’t tell you confidently that we won’t move up our estimate of the peak rate, again, at the next SEP. I don’t know what we’ll do. It will depend on future data. What we’re writing down today is our

best estimate of what we think that peak rate will be based on what we know. Obviously, if data the inflation data come in worse, that could move up. And it could move down if inflation data are softer.

Jeanna Smialek, New York Times.

Thanks for taking our questions. The SEP, like you mentioned, suggests that the Fed will be making another 3/4 percentage points worth of rate increases in 2023. I wonder if you would foresee that being in 25 basis point increments, 50 basis point increments, sort of how you see the speed playing out going forward. And then I wonder what you’re looking at as you determine when to stop.

CHAIR POWELL

Yeah. So, as I’ve been saying, as we’ve gone through the course of this year, as we lifted off and got into the course of year and we saw the how strong inflation was and how persistent, it was very important to move quickly. In fact, the speed, the pace with which we’re moving was the most important thing. I think now that we’re coming to the end of this year, we’ve raised 425 basis points this year and we’re into restrictive territory, it’s now not so important how fast we go. It’s far more important to think what is the ultimate level? And then it’s at a certain point, the question will become how long do we remain restrictive? That will become the most important question. But I would say the most important question now is no longer the speed. So and that applies to February as well. So I think we’ll make the February

decision based on the incoming data and where we see financial conditions, where we see the economy. And that’ll be the key thing but I mean, for that decision. But, ultimately, that question about how high to raise rates is going to be one that we make looking at our progress on inflation, looking at where financial conditions are, and making an assessment of whether policy is restrictive enough. I’ve told you today we have an assessment that we’re not at as restrictive enough stance, even with today’s move. And we’ve laid out our individual assessments of what we would need to do to get there. At a certain point, though, we’ll get to that point. And then the question will be how long do we stay there. And there, the strong view on the Committee is that we’ll need to stay there, you know, until we’re really confident that inflation is coming down in a sustained way. And we think that that will be some time. Now, why do I say that? If you look at you can break inflation down into three sort of buckets. The first is goods inflation, and we see now, as we’ve been expecting, really, for a year and a half that supply conditions would get better. And, ultimately, supply chains get fixed, and demand settles down a little bit and maybe goes back to services a little bit. And we start to see goods inflation coming down. We’re now starting to see that in this report and the last one. Then you go to housing services. We know the story there is that housing services, inflation has been very, very high and will continue to go up, actually, as rate as rents expire and have to be renewed, they’re going to be renewed into a market where rates are higher than they were when the original leases were signed. But we see that the new leases that are that the rate for new leases is coming down. So, once we work our way through that backlog, that inflation will come down sometime next year. The third piece, which is something like 55 percent of the index, PCE core inflation index, is non-housing-related core services. And that’s really a function of the labor market, largely, at the biggest cost by far in that sector is labor. And we do see a very, very strong labor market, one where we haven’t seen much softening, where job growth is very high, where wages are very high. Vacancies are quite elevated and, really, there’s an imbalance in the labor market between supply and demand. So that part of it, which is the biggest part, is likely to take a substantial period to get down. The other you know, the goods inflation has turned pretty quickly now after not turning at all for a year and a half. Now it seems to be turning. But there’s an expectation, really, that the services inflation will not move down so

quickly, so that we’ll have to stay at it so that we may have to raise rates higher to get to where we want to go. And that’s really why we are writing down those high rates and why we’re expecting that they’ll have to remain high for a time.

Howard Schneider with Reuters.

Thanks for taking the question. You describe GDP growth in the SEPs as moderate or modest, I believe. Yet, it’s really approaching stall speed. Half a percentage point is not much. You described labor market

unemployment rate as representing some softening. But it’s nearly a full percentage point rise, and that’s well in excess of what has historically been associated with recession. Why wouldn’t this be considered a recessionary projection by the Fed?

CHAIR POWELL

Well, I’ll tell you what the projection is. I don’t think it would qualify as a recession, though, because you’ve got positive growth. The expectations in the SEP are basically, as you said, which is we’ve got growth at a modest level, which is to say that a half a percentage point, that’s positive growth. It’s slow growth. It’s well below trend. It’s not going to feel like a boom. It’s going to feel like very slow growth, right. In that, in that condition, labor market conditions are softening a bit. Unemployment does go up a bit. I would say that many analysts believe that the natural rate of unemployment is actually elevated at this moment. So it’s not clear that those forecasts or inflation are really much above the natural rate of

unemployment. We can never identify its location with great precision. But that 4.7 percent is still a strong labor market. If you look you know, you’ve got the reports we get from the field are that companies are very reluctant to lay people off, other than the tech companies, which is, you know, a story unto itself. Generally, companies want to hold onto the workers they have because it’s been very, very hard to hire. So, you’ve got all these vacancies out there, far in excess of the number of employed people. That doesn’t sound like a — you know, a labor market where a lot of people will need to be put out of work. So that we you know, there are channels through which the labor market can come back into balance with relatively modest increases in unemployment, we believe. None of that is guaranteed, but that is what their forecasts reflects.

Nick Timiraos, Wall Street Journal.

Chair Powell, I want to follow up on Jeanna’s question. The decision to step down the pace of rate increase, the rate rises appears to have been socialized at your last meeting largely before the past two CPI reports showed inflation decelerating in line with the committee’s forecasts this year. You just now

talked about making decisions meeting by meeting and being mindful of the lags of policy. Does that mean, all things equal, you would feel more comfortable probing where the terminal rate is by moving in 25 basis point increments, including beginning at your next meeting?

CHAIR POWELL

So I haven’t made a judgment on what size rate hike to make at the last meeting. But, you know, what you said is broadly right, which is having moved so quickly and having now so much restraint that’s still in the pipeline, we think that the appropriate thing to do now is to move to a slower pace. And, you know, that will allow us to feel our way and you know, and get to that level, we think, and better balance the risks that we face. So that’s the idea. It makes a lot of sense, it seems to me, particularly if you consider how far we’ve come. But, again, I can’t tell you today what the actual size of that will be. It will depend on a variety of factors, including the incoming data, in particular, the state of the economy, the state of financial conditions.

NICK TIMIRAOS.

With the CPI report, if it did come out last week, do you think it would have changed some of those forecasts in today’s estimate?

CHAIR POWELL

No. Absolutely not. No. As a just a matter of practice, the SEP reflects any data that’s — that comes out during the meeting. And participants know that they have the they know that they can make changes to their SEP during the meeting, you know, well in advance of the press conference so that we’re not running around. But that’s not the case. It’s never the case that the SEPs don’t reflect an important piece of data that came in on the first day of the meeting.

Rachel Siegel from the Washington Post.

Thank you for taking our questions. I’m wondering if we could talk about the projection for the unemployment rate. Why has the Fed raised its unemployment projection? Is it because the model suggests that a higher terminal rate would automatically cause a higher unemployment rate? Or are you seeing signs that the labor market isn’t quite as strong as we think it is now?

Thanks.

CHAIR POWELL.

No. It’s not about the strength of the labor market. The labor market is clearly very strong. It is more just that, you know, by now, we had expected we’ve continually expected to make faster progress on inflation than we have, ultimately. And that’s why the that’s why the peak rate for this year goes up between this meeting and the September meeting. You see that you see the fact that we’ve made less progress than expected on inflation. So that’s why that goes up. And that’s why unemployment goes up because we’re having to tighten policy more. And so it didn’t go up by much in the meeting, I don’t think. But that’s the idea is slower progress on inflation, tighter policy, probably higher rates probably held for longer just to get to where you — the kind of restriction that you need to get inflation down to 2 percent.

RACHEL SIEGEL.

Do you have a sense of, in order to get to that number, how much of that could be caused by layoffs versus vacancies, trimming, or changes to the labor force population rate?

CHAIR POWELL.

It’s very hard to say. You know, there you can look at you can look at history, right. And history would, you know, would say that, in a situation like this, the declines in unemployment would be more meaningful, I think, than what you see written down there. But why do we think that is the case? So, I’ll give you a few reasons. First just is that there there’s this huge overhang of vacancies, meaning that vacancies can come down a fair amount. And we’re hearing from many companies that they don’t want to lay people off so that they’ll keep people because it’s been so hard. I mean, I think we’ve it feels like we have a structural labor shortage out there where there, you know, 4 million fewer people, a little more than 4 million who were in the workforce available to work than there’s demand for workforce. So, the fact that there’s a strong labor market, you know, means that companies will hold on to workers. And it means that it may take longer, but it also means that the costs in unemployment may be less, again, that we’re going to find out empirically. But I think that’s a reasonably possible outcome. And you do hear, you know, many, many labor economists believe that it is. So, we’ll see, though.

Colby Smith with the Financial Times.

How should we interpret the higher core inflation forecast for 2023 in the SEP? Does that not then suggest that the policy rate currently forecasted for next year should actually be higher than the 5.1 medium estimate penciled in?

CHAIR POWELL.

Well, I think that’s why one of the reasons it went up, was that core came in stronger this year, came in stronger this year. Yeah. What you see is our best estimate as of today, really, as of today for how high we need to raise rates to how much we need to tighten policy to create enough, you know, restrictive policy to slow economic activity and slow soften the labor market and bring inflation down through those channels. That’s all that is the estimate, best estimate we make today. And, as I mentioned, we’ll make another estimate for the next SEP. And we’ll, you know, of course, between meetings, we do the same

thing; but we don’t publish it.

Victoria Guida with Politico.

I wanted to make sure I understand specifically what’s going on in the SEP because you all expect rates to go higher, but you’re also more pessimistic about what inflation is going to look like next year. And I was just wondering, you know, given that we have seen some cooling in inflation, you know, is that primarily because of wage growth, that you expect wage growth to be sort of a headwind?

CHAIR POWELL.

We’re going into next year with higher inflation than we had thought, right. So, we’re actually moving down to the level that we’re moving down to next year is still a very large drop in inflation from where inflation is running now, well more than 1 percent change in inflation. But remember that the jump off point at the beginning of the year is higher. So, you know, we’re moving down still by a very large chunk. I don’t think it’s having I don’t think the policy is having any less effect. It’s just starting from a higher level at the end of So, we’re getting down. I believe the median is 3 1/2 percent. That would be that’s a pretty significant drop in inflation. And, you know, where’s it coming from? it’s coming from the goods sector, clearly. By the middle of next year, we should begin to see lower inflation from the housing services sector. And then, you know, the big question is, when we how much will you see from the largest, the 55 percent of the index, which is the nonhousing services sector. And, you know, that’s where you need to see we believe you need to see a better balancing of supply and demand in the labor market so that you have it’s not that we don’t want wage increases. We want strong wage increases. We just want them to be at a level that’s consistent with 2 percent inflation. Right now that if you put into if you factor in productivity estimates, standard productivity estimates, wages are running, you know, well above what would be consistent with 2 percent inflation.

Neil Irwin with Axios.

Some of your colleagues have been pretty explicit that they can’t imagine rate cuts happening in 2023. That’s certainly not implied by the SEP. But futures markets have priced in some easing in the back half of next year. What’s your view of the likelihood of any kind of rate cuts next year? What circumstances might make that plausible?

CHAIR POWELL.

You know, our focus right now is really on moving our policy stance to one that is restrictive enough to ensure a return of inflation to our 2 percent goal over time. It’s not on rate cuts. And we think that we’ll have to maintain a restrictive stance of policy for some time. Historical experience caution strongly against prematurely loosening policy. I guess I would say it this way: I wouldn’t see us considering rate cuts until the Committee is confident that inflation is moving down to 2 percent in a sustained way. So that’s the test I would articulate. And you’re correct. There are not rate cuts in the SEP for 2023.

Steve Matthews with Bloomberg.

Let me ask you about China. In the last few weeks, China has abandoned its COVID policy and been reopening pretty strongly. I’m wondering if you see that as disinflationary because you’re seeing supply chains improve or inflationary because it obviously brings a lot more demand globally and proves a global outlook for growth and for commodities prices.

CHAIR POWELL.

So you’re right. Those two things will offset each other. Weaker output in China will push down on commodity prices, but it could interfere with supply chains ultimately; and that could that could push inflation up in the West. It’s very hard to say, you know, how much, how those two will offset each other. And it doesn’t seem likely, actually, that the overall net effect would be material on us. But, to your point, China faces a very challenging situation in reopening. You know, we’ve seen waves of COVID all around the world can interfere with economic activity. China, a very critical manufacturing place for manufacturing and exporting. Their supply chain is very important. And China faces a reopening. They’ve you know, they’ve backed away from their COVID restriction policies that could be very significant increases in COVID. And we’ll just have to see. It’s a risky situation. It but, again, it doesn’t seem like it’s likely to have material overall effects on us.

Chris Rugaber, Associated Press.

Thank you for taking my question. I wondered if you could comment a bit more about yesterday’s inflation report. I mean,it showed inflation cooling in all three of the categories that you laid out at Brookings. Are you starting to see are you confident that you’re seeing real progress on getting inflation under control? Are you still worried it could slip into some kind of unentrenched, you know, upward

spiral? Thank you.

CHAIR POWELL.

Right. So the data that we’ve received so far for October and November, we don’t have the some of the we have some remaining data to get in November, but they clearly do show a welcome reduction in the monthly pace of price increases. As I mentioned in my opening statement, it will take substantially more evidence to give confidence that inflation is on a sustained downward path. So the way we think about this is this: This report is very much in line with what we’ve been expecting and hoping for. And what it does is it provides greater confidence in our forecast of declining inflation. As I mentioned, we’ve been

expecting significant forecasting significant declines in overall inflation and core inflation in the coming year. And this is the kind of reading that it will take to support that. So, really, this gives us greater confidence in our forecasts, rather than at this point changing our forecast. In terms of the pieces, we have been expecting goods inflation to come down as supply chain pressures eased. That’s happening now. Housing services, as I mentioned, there’s good news in the pipeline. As long as housing, new housing leases show declining inflation, that will show up in the measure around the middle of next year. So that should help. And the big piece, again, is core services, X housing, which is very important. And we have a ways to go there. You do see some beginning signs there. But, ultimately, that’s the big the more than half, as I mentioned, of PCE core index. And it’s very fundamentally about the labor market and wages. If you look at wages, look at the average hourly earnings number we got with the last payrolls report, you don’t really see much progress in terms of average hourly earnings coming down. Now there may be composition effects and other effects in that. So we don’t put we don’t put too much weight on any one report. These things can be volatile month to month. But we will be looking for wages moving, you know, down to more normal levels where workers are doing well and, ultimately, their gains are not being eaten up by inflation.

Michael McKee from Bloomberg Radio and Television.

There’s a little bit of a disconnect between the optimistic view you just expressed

about the economy and the changes that you’ve made in the SEP. And I’m wondering if you’re

reacting to the fact that the markets have loosened financial conditions, or if you feel the Fed

may be a little bit behind on inflation, whether the recent disinflation we’re seeing is transitory or

not and how this affects the idea of a soft landing if you’re projecting just half a percent growth

for this year.

CHAIR POWELL.

So if I think I got your question. So, you know, one thing is to say is I think our policies in getting into a pretty good place now. We’re restrictive, and I think we’re you know, we’re getting close to that level of sufficient, we think sufficiently restrictive. We laid out today what our best estimates are to get there. And, I mean, it boils down to how long do we think this process is going to take? And, of course, we welcome these better inflation reports for the last two months. They’re very welcome. But I think we’re

realistic about the broader project. So that’s all. That’s the point I would make. It’s you know, we see goods prices coming down. We understand what will happen with housing services. But the big story will really be the rest of it, and there’s not much progress there. And that’s going to take some time, I think my view and my colleagues’ view is that this will take some time. We’ll have to hold policy at a restrictive level for a sustained period so that, you know, two good you know, two good monthly reports are, you know, very welcome. Of course, they’re very welcome. But we need to be honest with ourselves that there’s, you know, inflation; 12-month core inflation is 6 percent CPI. That’s three times our 2 percent target. Now, it’s good to see progress. But let’s just understand we have a long ways to go to get back to price stability.

MICHAEL MCKEE. Well, do you think the soft landing is no longer achievable?

CHAIR POWELL.

No, I wouldn’t say that. No. I don’t say that. I mean, I would say this: You know, to the extent we need to keep rates higher and keep them there for longer and inflation, you know, moves up higher and higher, I think that narrows the runway. But lower inflation readings, if they persist in time, could certainly make it more possible. So I just I don’t think anyone knows whether we’re going to have a recession or not and, if we do, whether it’s going to be a deep one or not. It’s just it’s not knowable. And certainly, you know, lower inflation reports, were they to continue for a period of time, would increase the likelihood of a put it this way, of a return to price stability that involves significantly less, less of an increase in unemployment than would be expected given the historical record.

Brian Cheung, NBC News.

You warned Americans of pain earlier this year as the Fed hikes rates. But with the Fed now expected to raise rates higher than you thought when you first said that, just wondering where we are in that pain. How would you describe that to Americans if the projections on unemployment find themselves, that’d be 1.6 million Americans out of jobs?

CHAIR POWELL.

So the largest amount of pain, the worst pain would come from a failure to raise rates high enough and from us allowing inflation to become entrenched in the economy so that the ultimate cost of getting it out of the economy would be very high in terms of employment, meaning very high unemployment for extended periods of time, the kind of thing that had to happen when inflation really got out of control and the Fed didn’t respond aggressively enough or soon enough in a prior episode, you know, 50 years ago. So that’s really the worst pain would be if we failed to act. What we’re doing now is, you know, it’s raising

interest rates for people. And so people are paying higher rates on mortgages and that kind of thing. There will be some softening in labor market conditions. And I wish there were a completely painless way to restore price stability. There isn’t. And this is the best we can do. I do think, though, that and markets are pretty confident, it seems to me, that we will get inflation under control. And I believe we will. We’re certainly highly committed to do that.

Grady Trimble with Fox Business.

You’ve reiterated today and the Committee has reiterated its commitment to that 2 percent inflation

target. I wonder, is there ever a point where you actually reevaluate that target and maybe increase your inflation target if it is stickier than even you think it is?

CHAIR POWELL.

That’s just changing our inflation goal is just something we’re not thinking about, and it’s something we’re not going to think about. It’s we have a 2 percent inflation goal, and we’ll use our tools to get inflation back to 2 percent. I think this isn’t the time to be thinking about that. I mean, there may be a longer run project at some point. But that is not where we are at all. The Committee, we’re not considering that. We’re not going to consider that under any circumstances. We’re going to — we’re going to keep our inflation target at 2 percent. We’re going to use our tools to get inflation back to 2 percent.

Nicole Goodkind, CNN Business.

As you monitor wage growth and unemployment data, I wonder if you’re paying close attention to a sector or even income level? Like, how do you factor potential exacerbations of inequality into your risk calculations, especially given the K-shaped recovery of 2020?

CHAIR POWELL.

So the I would go back to the labor market that we had in 2018, ’19, ’20. So what that looked like was wage increases for the people at the lowest end of the income spectrum were the largest. The gaps between racial groups and gender groups were at their smallest in recorded history. That’s and that all of that because of a tight labor market, a tight labor market which had inflation running, you know, just a tick below 2 percent and the economy growing right at its potential. So that seems like something that would be really good for the economy and for the country, if we can get back to that. And so that’s what all of us want to do. We want to get back to us to a long expansion where the labor market can remain strong over an extended period of time. That’s a really good thing for workers in the economy. And we’d love to get back to that that’s what our goal is, you know, there’s in the near term, we have to use our tools to restore price stability. But we — you know, we can’t — what we have to think about is the medium and longer term. If you think about it, the country went through a difficult time, I think, much more difficult than we can think it would happen here. But it really set up our economy for several decades of prosperity. So price stability is something that really pays dividends for the benefit of the economy and the people in it over a very, very long period of time. And so, when it is lost, for whatever reason, it has to be restored and as quickly as possible, which is what we’re doing.

NICOLE GOODKIND. In the short-term, are you factoring in these exacerbations or potential exacerbations in the economy? Are you monitoring them?

CHAIR POWELL.

We do, yes. We absolutely do. We look at it’s our regular practice to talk about unemployment rates by different groups, including racial groups and that sort of thing. We do. We keep our eye on that.

Nancy Marshall-Genzer with Marketplace.

What would you do if the economy slows so much that we enter a recession before we see strong

consistent signs that inflation is slowing, in other words, stagflation?

CHAIR POWELL.

So I don’t want to get into too many hypotheticals. But, you know, we’ll it’s hard. It’s hard to deal with hypotheticals. So let me just say that we have to use our tools to support maximum employment and price stability. I’ve made it clear that right now, the labor market’s very, very strong, near a 50-year low where you’re at or above maximum employment. In 50-year low in unemployment, vacancies are very high, wages, nominal wages are very high. So the labor market’s very, very strong. Where we’re missing is on the inflation side. And we’re missing by a lot on the inflation side. So that means we need to really focus on getting inflation under control, and that’s what we’ll do. I think, as the economy heals, the two

goals come more into play. But right now, clearly, the focus has to be on getting inflation down.

Greg Robb from MarketWatch.

You spoke a little bit ago. You said that the U.S. looks — it looks like we have a structural labor shortage in the economy. Could you expand on that? Talk a little bit more about that. And, really, are you talking about getting Congress action on increasing, like, legal immigration, things like that?

Thank you.

CHAIR POWELL.

So what I meant by that with structural labor shortage is, if you look at where we are now, as I mentioned there, if you just look at demand for labor, you can look at vacancies plus people who are actually working. And then you can take supply of labor by are you in the labor market? Are you looking for a job or have a job? And you’re 4, more than 4 million people short. We don’t see despite very high wages and an incredibly tight labor market, we don’t see participation moving up, which is contrary to what we thought. So the upshot of all that is the labor market is actually it should it’s 3 1/2 million people at least

smaller than it should have been based on pre-pandemic. Just assume population and reasonable

growth and aging of the population, our labor force should be 3 1/2 million more than it is. And that it can they’re easy, lots of easy ways to get to bigger numbers than that if you go back a few more years. So why is that? Part of it is just accelerated retirements. People dropped out and aren’t coming back at a higher rate than expected. Part of it is that we lost a half a million people who would have been work close to half a million who would have been working died from COVID. And part of it is that migration has been lower. We don’t prescribe you know, it’s not our job to prescribe things. But, you know, I think if you ask businesses, you know, pretty much everybody you talk to says there aren’t enough people. We need more people. So I tried to identify that in my in a speech I gave a month ago, but I stopped short of telling Congress what to do because, you know, they gave us a job. And we need to, you know, do that job. Thanks.

Jennifer Schonberger with Yahoo! Finance.

You say you expect growth of just 1/2 percent next year, given that you’ve said the process of raising rates and getting inflation back under control will be painful. Have you had

discussions within the Committee and addressed how long and/or how deep of a recession you

would be willing to accept?

CHAIR POWELL.

No. I mean, what we do is we make — we make our forecasts, and we publish them quarterly. And, you know, if you look at those forecasts, those are forecasts for slow growth, for a softening labor market, by which I mean unemployment goes up but not a great deal. And you see inflation coming down. You see rates going up. You see inflation coming down. Those are those forecasts, and that’s really what they show. We’re not we of course, we don’t talk about, you know, this kind of a recession and that kind of a

recession. We just you know, we make those forecasts. The staff runs, and you will see this if you look at the old Tealbooks, runs alternative simulations of all different kinds at every meeting, and we look at those too. And those will explore different things. But that’s just, you know, upside and downside scenarios. Of course, that’s a responsible practice that we’ve carried on for many decades. But no, we don’t we haven’t asked ourselves that question.

Jean Yung with Market News.

I wanted to ask about the SEP again. If you’re reaching peak rates around 5 percent in the first half of next year and inflation starts to decline materially, that would seem to make the real rate gradually more restrictive. Is that something that’s built into the projections and into models? Is that something you would want to see?

CHAIR POWELL.

So we do know that. Of course, that’s something that we know we’d see. But, as I mentioned, that, you know, we wouldn’t I wouldn’t see the Committee cutting rates until we’re confident that inflation is moving down in a sustained way. That would be my test. I don’t see us as having a really clear and precise understanding of what the neutral rate is and what real rates are so that would mechanically happen like that. It would really it’ll be a test of for cutting rates, I think, in the event it’ll be a question of do we actually feel confident that inflation is coming down in a sustained way.

Thank you very much.